ABI December 2025: Architecture firm billings remain soft to end the year

Most firms have seen some stalled, delayed, or canceled projects over the last six months.

Weak business conditions at architecture firms persisted into 2025

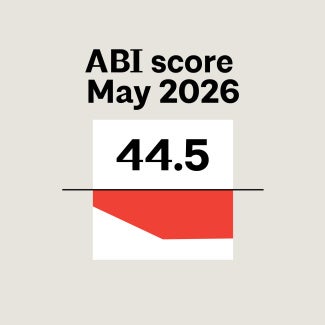

The AIA/Deltek Architecture Billings Index® (ABI) remained below the 50 threshold with a score of 48.5 for December (a score below 50 indicates declining firm billings). Architecture firm billings declined every month of 2025 and have declined every month except for three since October 2022. Fewer firms reported a decrease in billings in December than in recent months, but with inquiries into new work remaining weak, and the value of newly signed design contracts continuing to decline, a rebound is unlikely in the near future. However, backlogs at firms remain generally solid, averaging 6.3 months, with some extending as long as 8.6 months at large firms with annual billings of $5 million or more and 8.2 months at firms with an institutional specialization. Work in the pipeline at firms has generally held steady in recent years, despite fewer inquiries and a lower value of newly signed design contracts.

Regardless of the ongoing decline in billings at the majority of architecture firms, billings increased at firms located in the Midwest for the fourth consecutive month in December. While business conditions remain soft at firms in other parts of the country, billings have continued to strengthen at firms located in the Midwest over the last quarter. However, business conditions remained weak at firms of all specializations this month. Billings were softest at firms with a multifamily residential specialization, while firms with an institutional specialization reported a modestly slower decline than they experienced earlier in the year.

Conditions in the broader economy remain challenging

Conditions in the broader economy remained challenging in December. Nonfarm payroll employment added just 50,000 new positions for total growth of 584,000 for the year, 71% below 2024 nonfarm payroll growth of 2,000,000. Notably, federal government employment decreased by 277,000 positions, or 9.2%, in 2025. Architectural services employment continued to grow modestly in November, the most recent data available, adding 100 new positions. Total employment in the sector rose to 205,200, the highest level since June 2024, with nearly 2,000 new jobs added in 2025. Inflation remained stubborn in December as well, with the Consumer Price Index (CPI) increasing by 0.3% from November and by a total of 2.7% for the year. Increases in food, shelter, and energy prices were the primary contributors to the December increase. However, the cost of used cars and trucks and household furnishings declined for the month.

Most firms have experienced delayed, stalled, and/or canceled projects in recent months

With ongoing economic uncertainty, projects that are significantly delayed, on hold/indefinitely stalled, or canceled/abandoned remain an issue for architecture firms. This month, 90% of responding firm leaders reported that they have had projects that have been significantly delayed over the past six months, 84% have had projects that have gone on hold/indefinitely stalled, and 71% have had projects that were canceled/abandoned.

More than one-quarter of respondents (27%) reported that, over the past six months, the share of projects at their firm (on a dollar basis) that have been significantly delayed has increased, while 28% reported that the share of projects on hold has increased. While the share of firm leaders reporting that the share of projects at their firms that have been canceled in the last six months was lower, nearly one in five reported that it had increased in that period (16%). Firms located in the West and those with a multifamily residential specialization were most likely to report that the share of projects at their firms that have been delayed (38% and 37%, respectively) and/or put on hold has increased over the last six months (38% and 33%, respectively), while firms located in the West were most likely to report an increase in canceled projects (22%). On the other hand, firms located in the South were significantly less likely than those in other regions to report delayed projects in the last six months (15%).

However, firms reported that an average of 70% of their recent projects have been proceeding as normal, on a dollar basis. Firms reported that an average of just 5% of their projects have been canceled/abandoned, and 10% have been put on hold/indefinitely stalled. But firms reported that a greater share of their projects, on a dollar basis, have been significantly delayed recently, 16% on average.

When asked about the factors that have contributed to projects at their firm being delayed/stalled/canceled recently, the top reasons cited by responding firm leaders were client delays/indecision on key issues (55%), construction budget insufficient for project as currently conceived (49%), changing market conditions make clients nervous about proceeding (45%), financing problems (42%), and contractor bids coming in too high or schedules too long (41%). When asked to select the one most significant factor of those that contributed, one-fifth of respondents selected client delays/indecision, while 18% selected changing market conditions making clients nervous, and an additional 18% selected insufficient construction budget. While 22% of firms selected high interest rates as a contributing factor, just 2% selected it as the one most significant factor. Similarly, 19% selected material prices as a contributing factor, but just 3% selected it as the one most significant factor.

Finally, when asked about anticipated trends in delayed, stalled, or canceled projects over the first six months of 2026 as compared to the past six months, firm leaders were more likely to be optimistic than pessimistic. Nearly one-third (32%) anticipate that the trend will be lower over the coming six months, while just 8% expect there to be more stalled/delayed/canceled projects in the first half of the year. Firms located in the Northeast were more likely to expect the trend of delayed/stalled/canceled projects to increase however, with 12% indicating that sentiment.

- Join us for FREE at the next AIAU live webinar, Economic Update: Q3 2026 ABI Insights, on July 24, 2026, at 2 pm ET.

-

AIAThe AIA/Deltek Architecture Billings Index® (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construction activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates a decline in firm billings from the previous month.

AIAThe AIA/Deltek Architecture Billings Index® (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construction activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates a decline in firm billings from the previous month. -

AIAGraphs represent data from December 2024–December 2025.

AIAGraphs represent data from December 2024–December 2025. -

AIAGraphs represent data from December 2024 to December 2025 across the four regions. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows an increase; Below 50 shows a decrease. 3-month moving average.

AIAGraphs represent data from December 2024 to December 2025 across the four regions. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows an increase; Below 50 shows a decrease. 3-month moving average. -

AIAGraphs represent data from December 2024 to December 2025 across the three sectors. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows an increase; Below 50 shows a decrease. 3-month moving average.

AIAGraphs represent data from December 2024 to December 2025 across the three sectors. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows an increase; Below 50 shows a decrease. 3-month moving average. -

AIAPercentage of firms indicating one most significant factor contributing to projects at their firm being delayed/stalled/canceled recently.

AIAPercentage of firms indicating one most significant factor contributing to projects at their firm being delayed/stalled/canceled recently.

This month, Work-on-the-Boards participants are saying:

- “It is very strong for select clients, like aviation and sports.”—520-person firm in the Midwest, institutional specialization

- “Demand for future housing has skyrocketed due to so few projects in the design/permitting pipeline. While the financing markets have moved in a positive direction, everything is still very tentative and unpredictable.”—54-person firm in the West, multifamily residential specialization

- “We’re seeing some prospects emerge, but many are in wait-and-see mode.”—4-person firm in the South, commercial/industrial specialization

- “Conditions are slower than 2024, even though 2025 was a good year for us. Our clients are more cautious, and that means fewer RFPs for non-critical projects. Most of our current projects are related to much-needed infrastructure upgrades (mechanical systems, electrical switchgear, etc.).”—12-person firm in the Northeast, institutional specialization

Join the ABI Work-on-the-Boards panel to participate in our monthly survey. Open to architecture firm owners, principals, and partners. All participants get a free ABI subscription.

The monthly AIA/Deltek Architecture Billings Index is a leading economic indicator for nonresidential construction activity.

Deltek is the home of AIA MasterSpec®, powered by Deltek Specpoint. Deltek helps A&E firms boost efficiencies while improving collaboration and accuracy.

Nonresidential building construction reflects a K-shaped economy in 2026, marked by widening differences in performance across sectors.