ABI September 2025: Weakness persists at architecture firms

Nearly all firms report working on reconstruction projects over the last year.

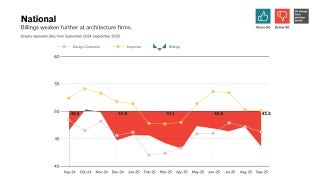

Business conditions at architecture firms remained weak in September

The AIA/Deltek Architecture Billings Index (ABI) score of 43.3 for the month is the softest reading since April and represents an increase in the share of firms reporting a decrease from August. In addition, inquiries into new projects remained flat for the second consecutive month, following growth over the summer, and the value of newly signed design contracts decreased for the 19th consecutive month. All of these indicators mean that the soft conditions that many architecture firms have been experiencing since late 2022 are likely to persist for the foreseeable future.

Firm backlogs soften

Recent revisions to work in the pipeline continue to erode as well. In the aftermath of the pandemic-induced downturn in 2020, architecture firm backlogs reached the highest levels we have seen since we started collecting that data regularly 15 years ago. Backlogs have gradually declined since the third quarter of 2022 and currently stand at an average of 6.1 months, down from 6.5 months at the beginning of the year. Backlogs are averaging just five months at firms with multifamily residential and commercial/industrial specializations, but stand at an average of eight months at firms with an institutional specialization. But despite the recent decrease in backlogs at firms, they still stand at levels nearly comparable to those before the pandemic.

Billings declined at firms in all regions of the country in September, except for firms located in the Midwest, where billings were essentially flat. Billings were softest at firms located in the West for the fourth consecutive month, where they have weakened the most over the last year. By firm specialization, business conditions were weakest at firms with an institutional specialization this month and continued to soften at firms with a commercial/industrial specialization, which reported conditions approaching growth over the summer.

Consumer confidence falls to lowest levels since spring

Due to the ongoing government shutdown, no updates to employment or inflation data for September are available. However, the Conference Board Consumer Confidence Index® sheds some light on business conditions in the broader economy in September. The index declined by 3.6 points to 94.2 in September (where 1985 equals 100), falling to its lowest level since April. Overall, the index remains well below pre-pandemic levels and significantly below the levels seen in 2021 and 2022. Concerns about current business conditions and job availability contributed to the decline this month, although optimism about future income increased. Additionally, overall confidence increased among consumers under 35, but decreased among those over 35. It seems likely that softer economic conditions will prevail in the aftermath of the government shutdown, but it may take a while before the data is released and we can assess the full impact.

An average of half of design billings are from reconstruction projects

This month, we asked firms about work on reconstruction projects to existing buildings (e.g., renovations, retrofits, rehabilitations, alterations, additions, and historic preservation) that their firms have performed over the last year. Overall, 97% of responding firms reported working on reconstruction projects over the past year. Firms located in the South (93%) and those specializing in multifamily residential development (93%) were least likely to report recent work on reconstruction projects. At firms that have worked on reconstruction projects in the last year, they estimated that an average of 50% of their firm’s total building design billings have been from these projects over the past year. This share was significantly higher at firms located in the Northeast (58%), where some of the oldest building stock in the country exists, than in the South (45%) and West (47%). Smaller firms also reported a much higher share of their billings from these projects, averaging 70% of total design billings at firms with annual billings of less than $250,000, compared to 40% at large firms with annual billings of $5 million or more.

Office buildings were by far the most commonly cited building type for which reconstruction projects were undertaken over the past year, cited by 53% of firms. Following office buildings were college/university education facilities (33% had reconstruction projects for this building type over the past year), government (30%), retail (28%), K-12 education (28%), multifamily residential (28%), and health care (27%).

The principal goals of reconstruction projects undertaken over the past year included basic updating and modernization of the building interior (cited by 74% of firms), upgrades to basic building systems (HVAC, lighting) (63%), upgrades to building shell (roof, facade, windows/doors, entrances) (63%), adaptive reuse or building conversion (61%), and tenant fit outs (54%). Basic updating and modernization was cited as the one single most important goal of recent reconstruction projects by 28% of responding firms, followed by adaptive reuse or building conversion (26%), and tenant fit-outs (16%). Tenant fit-outs were most commonly cited by firms with a commercial/industrial specialization (30% versus 15% of firms with a multifamily residential specialization and 8% of firms with an institutional specialization).

Finally, all firms were asked about their expectations for reconstruction projects in the future. Overall, two-thirds of responding firms (68%) expect that reconstruction projects as a share of total firm revenue will remain at about the same level over the coming years. More than one-quarter (28%) expect the share to increase, while just 4% expect it to decrease. Firms located in the South (34%) and large firms (35%) were significantly more likely to project that the share will increase in the coming years.

- Join us for FREE at the next AIAU live webinar, Economic Update: Q4 2025 ABI Insights, on Thursday, November 20, 2025, at 2pm ET.

-

AIAGraphs represent data from August 2024–August 2025.

AIAGraphs represent data from August 2024–August 2025. -

AIAGraphs represent data from September 2024–September 2025.

AIAGraphs represent data from September 2024–September 2025. -

AIAGraphs represent data from September 2024–September 2025 across the four regions. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; below 50 shows decrease. 3-month moving average.

AIAGraphs represent data from September 2024–September 2025 across the four regions. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; below 50 shows decrease. 3-month moving average. -

AIAGraphs represent data from September 2024–September 2025 across the three sectors. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; below 50 shows decrease. 3-month moving average.

AIAGraphs represent data from September 2024–September 2025 across the three sectors. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; below 50 shows decrease. 3-month moving average. -

AIAPercentage of firms, rating how serious of an issue they believe compensation for architectural positions is across the profession and for their firm.

AIAPercentage of firms, rating how serious of an issue they believe compensation for architectural positions is across the profession and for their firm.

This month, Work-on-the-Boards participants are saying:

- “Business conditions had been trending upward. However, now with the federal government shutdown, we are back into full blown uncertainty.”—31-person firm in the Midwest, institutional specialization

- “The sales market remains strong, although high construction costs are creating a headwind to projects being undertaken.”—5-person firm in the Northeast, residential specialization

- “We have a significant number of projects where our firm has been selected for the work, but the client has not yet authorized us to start. Just yesterday, two large projects were canceled entirely due to economic conditions.”—40-person firm in the West, institutional specialization

- “We are getting more calls for supporting MEP firms on their infrastructure projects, like air handler unit replacements and fire alarm replacements in hospitals.”—5-person firm in the South, commercial/industrial specialization

Join the ABI Work-on-the-Boards panel to participate in our monthly survey. Open to architecture firm owners, principals, and partners. All participants get a free ABI subscription.

The monthly AIA/Deltek Architecture Billings Index is a leading economic indicator for nonresidential construction activity.

Deltek is the home of AIA MasterSpec®, powered by Deltek Specpoint. Deltek helps A&E firms boost efficiencies while improving collaboration and accuracy.

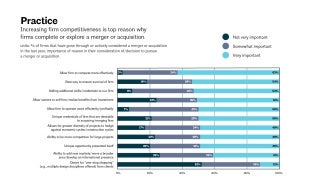

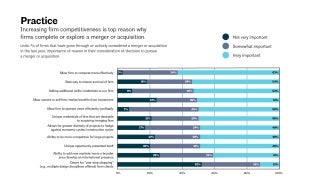

Few firms have engaged in a merger or acquisition over the last year.