ABI August 2025: Softness persists at architecture firms

Few firms have engaged in a merger or acquisition over the last year.

Softness persists at architecture firms

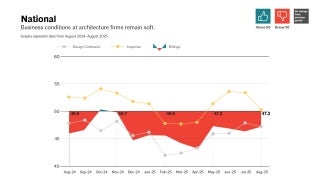

The AIA/Deltek Architecture Billings Index® (ABI) score was 47.2 for the month of August 2025. The share of firms reporting declining billings in August fell modestly from July, but overall, most firms continue to report a downward trajectory. In addition, inquiries softened in August and were essentially flat, after small increases over the previous three months. In addition, the value of new design contracts declined for the 18th consecutive month, the longest period of decline since we started collecting this data 15 years ago. This year has seen generally soft inquiries into new projects and a steady decrease in the value of newly signed design contracts, as clients remain cautious about committing to new projects. Without new work on the horizon, many firms will likely continue to experience declining billings in the coming months.

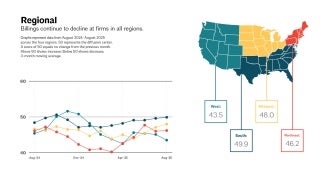

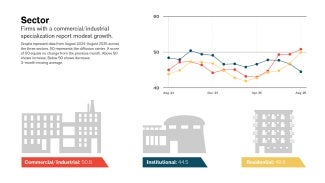

While business conditions remained soft at firms in most regions of the country in August, firms located in the South reported essentially flat conditions for the fourth consecutive month. In contrast, firms located in the West saw their billings soften this month, as they reported their weakest conditions in nearly two years. By specialization, firms with a commercial/industrial specialization reported modest growth in August for the first time in three years. And firms with a multifamily residential specialization have also seen improving conditions in the last few months and saw essentially flat billings this month. In contrast, business conditions have softened recently at firms with an institutional specialization to their lowest levels since 2020. Uncertainty with government budgets in recent months continues to cause uncertainty for many firms specializing in institutional facilities.

Signs of softness increase in the larger economy

Recent revisions to data show more softness in the broader economy this year than previously known. Nonfarm payroll employment was essentially flat in August, adding just 22,000 new jobs, and recent months have been revised downward, showing much smaller overall growth for the year. Architectural services employment increased modestly in July to 204,100 (the most recent data available). Employment in the industry has been generally flat over the last year and remains more than 3,500 positions below its post-pandemic peak employment of 207,700.

The Consumer Price Index (CPI) showed that inflation also ticked up modestly this month, increasing by 0.4% in August, the highest monthly increase since January. Inflation grew by 2.9% on an annual basis, an increase from average annual growth of 2.7% in recent months. With the Federal Reserve continuing to target an inflation rate of 2%, it lowered interest rates by 0.25 percentage points at its most recent meeting on September 17. Many experts expect them to lower rates by at least an additional 0.25 percentage points at one of their two remaining meetings before the end of the year.

Few firms have completed a merger or acquisition recently, but others are considering one

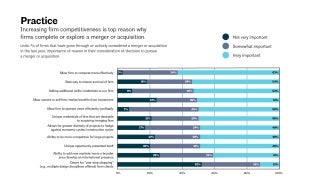

This month, we asked architecture firms about recent merger and acquisition activity at their firms and the latest trends in the industry. Overall, 72% of responding firm leaders reported that they have not considered or gone through with a merger or acquisition in the last year. Just 5% reported that they had actually gone through with a merger or acquired another firm in the last year, while 12% reported that they have actively considered being acquired by another firm, 7% that they have actively considered merging with another firm, and 6% that they have actively considered acquiring another firm (the remaining share of firm leaders reported some other response).

At firms that have either completed a merger or acquisition in the last year, or have actively considered one, the primary reason for doing so was to allow their firm to compete more effectively (rated as a very important reason by 63% of responding firm leaders). Other reasons rated as very important by more than half of responding firm leaders include that it was the best way to ensure the survival of the firm (54%), to add additional skills/credentials to their firm (53%), and to allow the firm owners to sell the firm/realize benefits from their investment (51%). Other top reasons included increasing firm profitability, unique attributes of the firm, shoring up against economic uncertainty, and expanding to new markets.

Of all responding firm leaders this month, the majority find it unlikely that they will be acquired by or merge with another firm over the next 3–5 years, with 36% saying that it is not at all likely, and an additional 28% saying that it is not very likely. Just 5% said that it is very likely, and that share is slightly higher for large firms (7%) and those with a commercial/industrial (8%) and multifamily residential specialization (7%). Responding firm leaders were even less likely to anticipate that their firm would acquire another firm in the next 3–5 years, with nearly half (47%) saying that it is not at all likely and an additional 23% saying that it is not very likely. Overall, 5% said that it is very likely, although that jumps significantly for firms located in the Midwest (12%) and at large firms (13%).

Finally, when asked about overall trends in the industry, nearly two-thirds of responding firm leaders (63%) expect merger and acquisition activity among U.S. architecture firms to increase over the coming 3–5 years. Less than 1% expect that it will decrease, while 18% expect that it will remain at current levels, and 18% say that they either don’t know or indicated some other response. Firm leaders expect that architecture firm acquisitions of/mergers with other architecture firms will by far be the most common type of merger and acquisition activity over the next 3–5 years, with nearly half (48%) selecting it. Just 14% expect that nonarchitecture firm (e.g., interior design, planning, engineering, construction) acquisitions of/mergers with architecture firms will be the most common activity, and 13% expect that architecture firm acquisitions of/mergers with other nonarchitecture firms (e.g., interior design, planning, engineering, construction) will be the most common activity (the remaining 26% said that they either don’t know or indicated some other response).

- Join us for FREE at the next AIAU live webinar, Economic Update: Q4 2025 ABI Insights, on Thursday, November 20, 2025, at 2pm ET.

-

AIAGraphs represent data from August 2024–August 2025.

AIAGraphs represent data from August 2024–August 2025. -

AIAGraphs represent data from August 2024–August 2025.

AIAGraphs represent data from August 2024–August 2025. -

AIAGraphs represent data from August 2024–August 2025. across the four regions. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; below 50 shows decrease. 3-month moving average.

AIAGraphs represent data from August 2024–August 2025. across the four regions. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; below 50 shows decrease. 3-month moving average. -

AIAGraphs represent data from August 2024–August 2025 across the three sectors. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; below 50 shows decrease. 3-month moving average.

AIAGraphs represent data from August 2024–August 2025 across the three sectors. 50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; below 50 shows decrease. 3-month moving average. -

AIAPercentage of firms, rating how serious of an issue they believe compensation for architectural positions is across the profession and for their firm.

AIAPercentage of firms, rating how serious of an issue they believe compensation for architectural positions is across the profession and for their firm.

This month, Work-on-the-Boards participants are saying:

- “Proposal activity has increased but contract signatures are weak. Still far too much uncertainty for investors to pull the trigger on larger projects.”—171-person firm in the West, commercial/industrial specialization

- “RFPs and RFQs have substantially decreased in amount. Project sizes are generally smaller in nature. Firms that would not have historically pursued small-scale work are pursuing those projects now.”—250-person firm in the Midwest, institutional specialization

- “Our firm has seen a significant increase in multifamily projects, starting with a great emphasis on getting projects shovel-ready to start construction.”—39-person firm in the South, residential specialization

- “Slow but appear to be increasing opportunities in fall 2025 into 2026.”—20-person firm in the Northeast, institutional specialization

Join the ABI Work-on-the-Boards panel to participate in our monthly survey. Open to architecture firm owners, principals, and partners. All participants get a free ABI subscription.

The monthly AIA/Deltek Architecture Billings Index is a leading economic indicator for nonresidential construction activity.

Deltek is the home of AIA MasterSpec®, powered by Deltek Specpoint. Deltek helps A&E firms boost efficiencies while improving collaboration and accuracy.

Most firms have seen some stalled, delayed, or canceled projects over the last six months.