ABI December 2022: Firm billings end the year softly

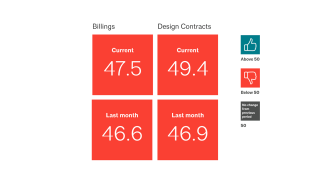

Architecture firm billings end 2022 on a soft note. The December ABI score of 47.5 is a modest improvement over the November score of 46.6, meaning slightly fewer firms reported a decline in firm billings.

Four in ten firm leaders report seeing an increase in delayed projects at their firm

Architecture firms reported ongoing softness in business conditions to close out 2022, as firm billings declined for the third consecutive month in December. However, the ABI score of 47.5 for the month is a modest improvement over the November score of 46.6, meaning that slightly fewer firms reported a decline in billings this month (a score below 50 indicates declining billings). While the value of new design contracts also declined for the third month in a row in December, the pace of that decline slowed as well. And inquiries into new projects continued to grow at a modest pace at the majority of architecture firms this month. Firms also continued to report robust project backlogs of 6.7 months, on average. While this is lower than the project backlogs throughout much of 2022, it is still higher than it was one year ago at the end of the fourth quarter of 2021.

Business conditions remained soft across the country in December, as billings declined in all regions for the second consecutive month. Conditions remained softest at firms located in the West and Northeast regions. Billings also declined at firms of all specializations this month, with the weakest conditions reported at firms with a multifamily residential specialization. Even firms with an institutional specialization are now seeing a more significant decline in billings, despite reporting strong growth just four months ago.

Industry employment hits a high point despite recession concerns

Despite ongoing concerns about a potential recession, conditions in the broader economy remained largely positive at the end of 2022. Total nonfarm payroll employment grew by another 223,000 positions in December, for total growth of 4.5 million positions in 2022. And architectural services employment added a strong 2,000 new positions in November (the most recent data available), following modest declines in September and October. Employment in the industry currently stands at a new high point since the Great Recession.

Consumer confidence also rebounded in December, following two months of declines, according to the Conference Board Consumer Confidence Index ®. That index now stands at its highest level since April 2022, and consumers reported that they are now generally less pessimistic about the next six months due to slowing inflation and lower gas prices in particular.

Stalled, delayed, and canceled projects of concern to firm leaders

For this month’s special practice questions, we asked architecture firm leaders for an update on the status of stalled, delayed, and canceled projects at their firms. When last asked about this subject in September 2022, 14% of firm leaders indicated that stalled/delayed/canceled projects were a serious issue at their firm, while 28% reported that it was a somewhat serious issue. When asked about affected projects now, 39% of firm leaders indicated that the share of significantly delayed projects at their firm has been increasing over the last six months, while 30% reported that the share of indefinitely stalled projects has been increasing, and 21% indicated that the share of canceled projects has been increasing.

Overall, firms reported that an average of 13% of the projects at their firm over the past six months have been significantly delayed, 6% have been indefinitely stalled, and 3% have been cancelled. Firms with a multifamily residential specialization have been most significantly impacted, as they reported that an average of 18% of their projects have been significantly delayed, in contrast to 15% of projects at firms with a commercial/industrial specialization and 9% of projects at firms with an institutional specialization. Firms located in the Northeast and West regions also reported a higher share of significantly delayed projects than firms in other regions.

Finally, when asked what they anticipate will be the trend for delayed, stalled, or cancelled projects over the first six months of 2023 as compared to the past six months, more than half of firm leaders (55%) indicated that they expect it to remain about the same. One quarter of firms expect to see fewer delayed, stalled, or cancelled projects, although 20% expect to see more. However, just 2% of firms indicated that they expect the share of stalled, delayed, or cancelled projects to be significantly higher over the next six months, in contrast to 9% that expect the share to be significantly lower.

What ABI December 2022 Work-on-the-Boards participants are saying

- “There are still opportunities for work, but clients are conscientious about rising interest rates. The offset to that is that contractors are starting to reach out for work for the first time in a couple of years, and there is some competition in the marketplace again.”

—17-person firm in the West, institutional specialization - “Infrastructure and repair projects are moving forward, while renovations, additions, or new buildings are in the stalled or canceled categories.”

—5-person firm in the Northeast, commercial/industrial specialization - “Softening. Still quite busy, but a significant number of new projects are on hold or have slowed dramatically.”

—27-person firm in the South, residential specialization - “Business remains consistent, although some canceled or delayed projects have provided a more competitive environment. Firms are focusing on building a backlog, and owners are looking at tightening their project expenditures.”

—12-person firm in the Midwest, commercial/industrial specialization

Want to contribute to a future ABI?

Join the ABI Work-on-the-Boards panel to participate in our monthly survey. Open to architecture firm owners, principals, and partners. All participants get a free ABI subscription.

The monthly AIA/Deltek Architecture Billings Index is a leading economic indicator for nonresidential construction activity.

Get the ABI delivered to your inbox monthly plus access to historical data for $369/year. Free for AIA members and Work-on-the-Boards survey participants.

Nearly half of firms have worked on projects that have characteristics of resilient design over the past five years.

Nonresidential building construction reflects a K-shaped economy in 2026, marked by widening differences in performance across sectors.