ABI July 2023: Architecture firm billings remain flat

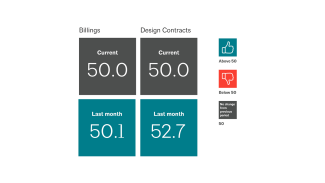

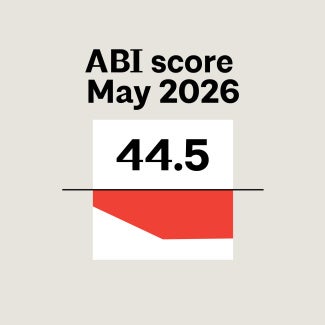

Billings at architecture firms remained flat in July with an ABI score of 50.0—meaning the share of firms that reported a decrease in their billings equaled the share of firms that reported an increase in their billings.

Four in 10 firm leaders currently consider their firms to be understaffed

Billings at architecture firms remained flat in July, with an AIA/Deltek Architecture Billings Index® (ABI) score of 50.0 for the month. A score of 50.0 means that the share of firms that reported a decline in their billings in July is equal to the share of firms that reported an increase in their billings for the month. Inquiries into new projects continued to grow, but at a slightly slower pace than in the last two months. However, the value of newly signed design contracts was flat in July, which means that firms saw fewer clients committing to projects than they had in the previous two months.

While billings were flat nationally, firms located in the Midwest continued to report improving business conditions in July, marking the ninth consecutive month of growth for firms located in the region. Firms located in all other regions of the country saw modest declines in billings, most notably at firms located in the South, which had previously seen three months of growth. Business conditions also improved at firms with both commercial/industrial and institutional specializations in July, with firms with a commercial/industrial specialization reporting their strongest billings in more than a year. Billings remained very soft at firms with a multifamily residential specialization, where it has now been a year since they last reported growth.

Architectural services employment continues to grow

In the broader national economy, conditions remained generally positive in July. The Conference Board’s Consumer Confidence Index rose to its highest score in two years, buoyed by consumer perceptions of more plentiful jobs and lower inflation. Consumers also reported increasingly optimistic expectations for the next six months, despite the fact that many still expect a recession. Nonfarm payroll employment also continued to grow in July, with 187,000 new positions added. Construction employment continued to strengthen, with a net total of 19,000 new jobs added. And architectural services employment continued to grow as well, with an additional 1,100 new positions added in June (the most current data available). Through the first six months of the year, the industry has added a total of 3,600 new positions.

Large firms least likely to consider their firms to be appropriately staffed

With staffing remaining an issue at many architecture firms, this month we asked firm leaders about their current architecture staffing levels. Overall, slightly more than half of responding firm leaders (53%) indicated that they consider the architecture staff at their firm to be appropriately staffed at present, while 40% reported that they are understaffed, and just 7% indicated that they are currently overstaffed. Large firms were the least likely to consider their firm to be appropriately staffed (41%), with 14% considering themselves overstaffed and 45% considering themselves understaffed. Firms located in the South, where billings have been the strongest recently, were more likely than firms in other regions to consider themselves understaffed (48%). On the other hand, firms with a multifamily residential specialization, where business conditions have been soft for the last year, were more likely than firms of other specializations to consider themselves overstaffed (10%) or appropriately staffed (61%), with just 28% reporting that they are understaffed.

Responding firms tended to be somewhat larger than the average architecture firm, with respondents indicating that they currently have an average of 25 full-time equivalent (FTE) architecture positions at their firm. Firms located in the Midwest reported the highest average number of FTE architecture positions (31), as did firms with an institutional specialization (27), and firms with annual billings over $5 million (57). Firms that consider themselves to be understaffed at present reported that they are understaffed by an average of 4 FTE architecture positions at present. That number was modestly higher for larger firms, which reported being understaffed by an average of 7 FTE architecture positions. Firms that consider themselves to currently be overstaffed reported that they are overstaffed by an average of 4 FTE architecture positions at present, while firms with a commercial/industrial specialization reported being overstaffed by an average of 6 FTE architecture positions currently.

What ABI July 2023 Work-on-the-Boards participants are saying

- “We are seeing softer inquiries/proposals sent in recent months, but still have a strong backlog and pipeline.” —200-person firm in the West, commercial/industrial specialization

- “The public sector has slowed down significantly. Hoping it is just the summer slowdown and things start to pick back up in the fall.” —6-person firm in the Northeast, institutional specialization

- “Busy, but financing is killing projects. Bank loans have almost stopped.” —52-person firm in the South, residential specialization

- “Accounts receivable are rising past 60 days to over 90. Project delays due to funding and scaled back scopes because of interest rates may lead to layoffs if we can’t find other opportunities.” —10-person firm in the Midwest, commercial/industrial specialization

Join the ABI Work-on-the-Boards panel to participate in our monthly survey. Open to architecture firm owners, principals, and partners. All participants get a free ABI subscription.

The monthly AIA/Deltek Architecture Billings Index is a leading economic indicator for nonresidential construction activity.

Deltek is the home of AIA MasterSpec®, powered by Deltek Specpoint. Deltek helps A&E firms boost efficiencies while improving collaboration and accuracy.

Nearly one quarter of firms report being currently understaffed.

This report reveals how a profession of 116,000 licensed architects enables $693 billion in construction value, supports millions of jobs, and generates a powerful multiplier effect across the