July 2025 Consensus Construction Forecast

Nonresidential building spending to remain sluggish through 2026, with no turnaround in sight.

No turnaround in sight for spending on nonresidential buildings

There is some good news and some bad news in the latest outlook for nonresidential construction spending on buildings, according to the latest AIA Consensus Construction Forecast. First the good news: In spite of stubbornly high long-term interest rates, inflation rates stalled above the Federal Reserve Board’s target, falling consumer confidence scores, disappointing levels of home building activity, rising tariff rates for many inputs to construction, and construction labor shortages exacerbated by restrictive immigration policies, the outlook for the remainder of the year and into 2026 is largely unchanged from where it was at in the beginning of the year.

The bad news: The outlook for spending entering the year was very pessimistic.

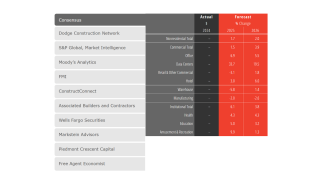

The consensus is that overall spending on nonresidential buildings not adjusted for inflation will increase only 1.7% this year and grow very modestly to just 2.0% next year. The commercial sector outlook is about on par with the broader industry, with a projected 1.5% increase this year rising to 3.9% in 2026. Spending on the construction of manufacturing facilities—the industry bright spot in recent years—is expected to decline 2.0% this year, with an additional decline of 2.6% next year. Institutional facilities are expected to be the strongest sector with projected gains of 6.1% this year and another 3.8% in 2026.

View interactive data from the Consensus Construction Forecast

An economic slowdown is emerging

Entering the year, the economy was expected to grow about 2%, with the probability of a recession over the coming twelve months estimated at 22%, according to the Wall Street Journal’s quarterly economic forecasting survey in January. However, since then, the outlook for the year has deteriorated. There is a growing list of threats to the economy, including tariffs, labor market implications of federal immigration policy, and federal job losses and spending cuts. The seriousness of these threats was reinforced by a negative GDP reading in the first quarter, even though the downturn was mostly driven by a surge in imports to beat the tariffs.

Ever-changing tariff policy has created unusually high levels of uncertainty across the economy. Not knowing what products will cost in the future, whether they will be available, how these changes might affect their supply chain, and whether they will provoke a trade war with the exporting countries are all questions that the AEC industry is asking before proceeding with planned projects.

A current concern is the extent to which tariffs are inflationary. With a few exceptions to date, consumer prices and producer prices have not increased much with the imposition and threatened imposition of tariffs. While this may change, recent research published by the National Bureau of Economic Research concludes that transitory tariffs are neither inflationary nor contractionary (generating an economic downturn). This suggests that if current tariffs are a negotiating mechanism that may be lowered or eliminated in the near future, they may not be a major headwind to the economy.

Regardless of the extent of their longer-term impact, tariffs have greater potential for disruption to some construction sectors than others. Analysis conducted by Wells Fargo Economics on Commerce Department data concludes that while imports account for about 10% of construction inputs by value across the entire industry, they account for about 75% more than the industry average for education and health care facilities, about a third less than the industry average for commercial facilities, and 50% less for residential projects.

An even greater concern than tariffs is the impact that immigration policy might have on labor markets in general and on construction specifically. With tight labor markets, a reversal or even a slowdown in immigration trends could have a dramatic impact. The Associated General Contractors of America (AGC) and the Associated Builders and Contractors (ABC) each estimate that there is an almost half million worker shortage nationally in the construction industry. The National Association of Home Builders estimates the shortage to be closer to 750,000.

While this estimated worker shortfall is a concern, even retaining the current immigration workforce in construction is becoming a significant challenge. There are currently about 12 million payroll and self-employed workers in the construction industry. About three million of these workers are foreign-born, which works out to a quarter of all workers in the industry, but about a third of craft workers—estimates of the share of foreign-born construction workers who are undocumented run as high as one-half. The share of undocumented immigrants in the construction workforce is slightly higher than the share in agriculture, and significantly higher than for any other industry.

As a result, concern over the potential deportation of undocumented workers is a major industry concern. Also, though, there is the fear that many documented workers may decide to either drop out of the labor force or even leave the country due to the perceived hostile political environment. Additionally, given added restrictions, fewer potential immigrants are likely to attempt to come to the U.S., further adding to workforce woes for the industry.

A final threat to more robust economic growth is the potential for federal spending cutbacks. The magnitude of the cutbacks is still unfolding, but job losses are expected to be hundreds of thousands of positions. Additionally, efforts are underway to reverse almost $10 billion in previously approved spending, a so-called rescissions package.

A slowdown in key growth sectors

Much of the overall growth in nonresidential building spending in recent years has come from a few key sectors, namely manufacturing aided by funding under the Infrastructure Investment and Jobs Act, the CHIPS and Science Act, and the Inflation Reduction Act; warehouses given the dramatic rise in e-commerce during the pandemic; and data centers to fuel the investment in artificial intelligence. However, we’ve seen or are currently seeing a significant slowdown in the largest two of these sectors.

There was over $230 billion in spending on manufacturing facilities in 2024, a 20% increase over 2023 levels. However, the outlook is for a modest cutback in spending this year and next. The consensus is that spending on manufacturing facilities will decline by 2.0% this year, and an additional 2.6% in 2026. For warehouse facilities, the pandemic-induced acceleration peaked in 2022 due to overbuilding, and spending has been slowing since. Last year saw an almost 20% decline in spending on warehouses, a trend that is expected to continue with another 5.8% decline in spending this year, before a modest 1.4% rebound next year. The unprecedented growth in spending on data centers, in contrast, is expected to continue at an elevated pace. After increasing by more than 50% last year, spending is expected to grow by another 33% this year and by an additional 20% next year. However, even in this sector, there are growing concerns that electrical equipment shortages, power requirements, and community opposition may slow the pace of growth.

Focus returns to traditional nonresidential building sectors

With the easing of some of the “high-flying” sectors, emphasis will return to the core sectors. On the commercial side, spending in the office category has been hampered by remote work that has produced national vacancy rates approaching 20%. Spending by building owners to make the space more desirable has spurred reconstruction spending, but not enough to offset the decline in new construction. Data centers have kept the overall category afloat because the U.S. Census Bureau classifies these facilities within the broader office category. However, netting out spending on data centers, spending on offices is expected to decline 3.6% this year, and another 2.0% next year.

Spending on retail facilities has been weak due to growth in e-commerce. More recently, however, the decline in warehouse spending—much of which is included in the broader retail category—has pulled down these totals. Net of the warehouse spending, the retail category is expected to see less than a 1% decline in spending this year before reversing to 2.0% growth next year.

The hotel sector saw steep declines in spending in the early days of the pandemic, but an increase in travel has benefited the outlook for these facilities. The forecast is for a 3.0% growth in spending this year and an additional increase of 6.0% in 2026.

Institutional sector facing its own headwinds

Entering this year, spending on institutional facilities was expected to outperform both the commercial and industrial sectors over the 2025-2026 period. While reasonably healthy growth is still expected, concerns are rapidly mounting.

For the health care sector, federal spending cuts to key funding programs like Medicaid and the Children’s Health Insurance Program (CHIP) will reduce spending on health care facilities. Spending is still projected to increase 4.3% both this year and next, but there is a higher degree of uncertainty that will remain until final programmatic decisions are made.

The outlook for the education market is a bit more complicated. Education is the largest institutional sector, accounting for over a third of all spending in this category. However, there are three major areas of concern regarding the outlook:

The first has to do with reductions in federal spending on health care research. Much of this research is conducted through colleges and universities, so a reduction in research funding will reduce the need for research facilities at these institutions.

Secondly, about 6% of the total U.S. higher education population is international students. At some institutions, the share is much higher. For example, at Harvard University, international students account for about a quarter of their enrollment. So, greater restrictions on visas for international students will reduce enrollments and therefore the need for education facilities.

Finally, longer-term demographic trends are not favorable for education construction. The Census Bureau estimates that the size of the under-18 population in the U.S. will decline by over three million persons, or by 4.3%, over the next ten years. This will reduce the need for secondary school facilities. So, overall spending on nonresidential buildings is expected to see growth over the next 18 months, but the risks of a downturn are growing.

Nearly half of firms have worked on projects that have characteristics of resilient design over the past five years.

Nonresidential building construction reflects a K-shaped economy in 2026, marked by widening differences in performance across sectors.