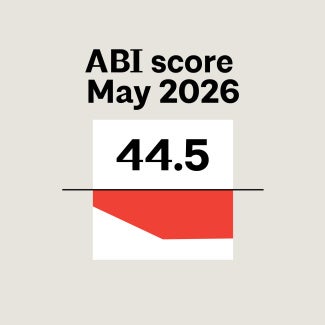

ABI March 2023: Business conditions improve slightly

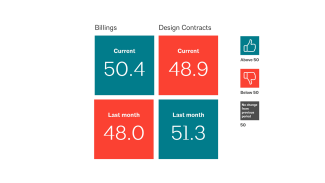

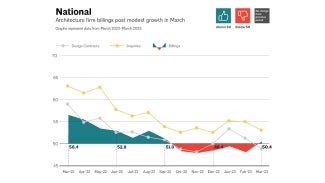

The Architecture Billings Index® (ABI) score of 50.4 in March 2022 indicates a slight majority of firms reported an increase in billings—an improvement in business conditions following declining billings during the last five months.

Architecture firm clients place moderate priority on health, resilience, & equity

Business conditions at architecture firms saw a slight improvement in March, following declining billings during the last five months. The AIA/Deltek Architecture Billings Index (ABI) score of 50.4 for the month indicates that a slight majority of firms reported an increase in their firm billings this month. In addition, backlogs at architecture firms ticked back up to an average of 6.9 months in the first quarter of 2023, after declining slightly in the fourth quarter of 2022. However, the pace of growth of inquiries into new projects at firms slowed in March, while the value of new design contracts declined for the first time in four months. This likely reflects the ongoing concern among clients about committing to new projects due to lingering uncertainty about interest rates and inflation.

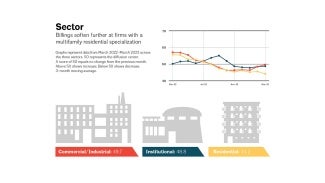

Billings continued to decline at firms in most regions of the country in March, with only those firms located in the Midwest continuing to report growth, as has been the case for the last five months. Business conditions also remained soft at firms of all specializations, as firms with a multifamily residential specialization saw conditions weaken to the lowest level since the early days of the pandemic. Only firms with a mixed specialization, meaning that they do not receive a majority of their billings from any one category, continued to report billings growth

Architecture services employment has remained flat since November

In the broader economy, there continue to be generally positive signs of growth, despite some ongoing uncertainty. Nonfarm payroll employment continued to rise in March, adding 236,000 new positions for total growth of 1,034,000 in the first quarter of the year. Architecture services employment increased by 400 positions in February, the most recent data available, nearly offsetting the industry’s losses from January. Overall, though, employment in the sector has been essentially flat since last November, with only small fluctuations from month to month.

Inflation continued to moderate in March as well, with the Consumer Price Index (CPI) rising by just 0.1% from February. However, inflation remains relatively high on average, at 5.0% higher than the level it was at one year ago. While energy prices declined and food prices remained stable this month, shelter prices increased 0.6% from February and are currently up by 8.2% from last year. Despite these signs of moderation, the Federal Reserve is projected to raise interest rates by another 0.25% at their next meeting in early May, although experts predict that they may pause at the 5.0–5.25% level after that, to see if that leads to greater moderation in inflation.

Most clients interested AIA Framework criteria

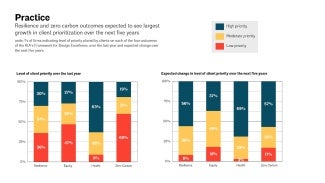

The special practice questions this month asked responding architecture firms about the level of priority that their clients generally place on the four outcomes of AIA’s Framework for Design Excellence in setting directions and outcomes for their design work, both over the last year and over the next five years. On average, responding firms reported that most of their clients placed at least moderate priority on outcomes related to issues of health1, resilience2, and equity3, with 63% of firms indicating that their clients placed a high priority on issues related to health for projects over the last year. Although firms indicated that 60% of their clients placed a lower priority on outcomes related to zero carbon4, that share is expected to flip over the next five years, with 57% reporting that they expect that it will become a high-priority issue for clients over that period. Outcomes related to health and resilience are also expected to continue increasing in client priority over the next five years (indicated by 69% and 56% of firms, respectively), while outcomes related to equity are expected to remain at the same level of priority as today (45% of firms) or become as higher priority (37% of firms).

Firms with an institutional specialization reported that their clients were most likely to place a higher priority on outcomes related to health and resilience over the last year (73% and 39%, respectively), although firms with a multifamily residential specialization also reported that their clients placed a high priority on health outcomes in projects during that period (66%). Over the next five years, firms with an institutional specialization expect that their clients will continue to prioritize these issues, while firms with a multifamily residential specialization also indicated that they expect their clients to place higher priority on outcomes related to both health (69%) and zero carbon (64%) in the future.

- Health: Good design supports health and well-being for all people, considering physical, mental, and emotional effects on building occupants and the surrounding community.

- Resilience: The ability of a system and its component parts to anticipate, absorb, accommodate, or recover from the effects of a hazardous event in a timely and efficient manner, including through ensuring the preservation, restoration, or improvement of its essential basic structures and functions.

- Equity: Equity is the state in which everyone is treated fairly and involved in making decisions regarding the potentially harmful consequences of industrial and governmental operations and policies.

- Zero carbon: Working toward achieving a zero-carbon future, to eliminate whole building lifecycle carbon emissions: the sum of both embodied and operational carbon.

What ABI March 2023 Work-on-the-Boards participants are saying

- “Business conditions remain surprisingly strong, with projects continuing to start even in the face of more costly development. Our backlog has increased by 50% over the last 40 days.” —8-person firm in the West, institutional specialization

- “High interest rates, high inflation, and construction cost escalation, along with tightening credit availability, is impacting the viability of many commercial developer projects in the multifamily and hospitality sectors. We expect to see projects in design in both sectors begin to hit pause, or get shelved altogether, in the coming months.” —90-person firm in the South, mixed specialization

- “The entire Columbus, OH metropolitan area is experiencing a significant increase in design and construction activity, based in large part on the federal government’s CHIPS and Science Act of 2022.” —30-person firm in the Midwest, commercial/industrial specialization

- “Business conditions are in flux based on interest rates and the availability of money.” —64-person firm in the Northeast, residential specialization

Join the ABI Work-on-the-Boards panel to participate in our monthly survey. Open to architecture firm owners, principals, and partners. All participants get a free ABI subscription.

The monthly AIA/Deltek Architecture Billings Index is a leading economic indicator for nonresidential construction activity.

Deltek is the home of AIA MasterSpec®, powered by Deltek Specpoint. Deltek helps A&E firms boost efficiencies while improving collaboration and accuracy.

Nearly one quarter of firms report being currently understaffed.

This report reveals how a profession of 116,000 licensed architects enables $693 billion in construction value, supports millions of jobs, and generates a powerful multiplier effect across the