ABI April 2023: Firm business conditions soften again

Business conditions continued to soften at architecture firms in April, as the Architecture Billings Index® score fell below 50 (48.5). Although new projects are continuing to come into firms, concern about various economic factors remains.

Most firms saw strong profitability in 2022 and expect equal or higher levels in 2023

Business conditions softened at architecture firms in April, as the AIA/Deltek Architecture Billings Index (ABI) score fell back below 50 (an ABI score below 50 indicates in a decline in firm billings). Excluding the slight growth seen in March, billings at architecture firms have declined every month since last October. While inquiries into new work continued to grow in April, the pace of growth remained relatively slow, and the value of new signed design contracts was essentially flat for the month. Although new projects are continuing to come into firms, concern about a variety of factors remains, including interest rates, financing, and the lingering potential for a recession.

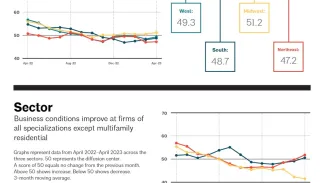

For the sixth consecutive month, only firms located in the Midwest saw billings growth in April. Business conditions remained sluggish at firms in other regions. By firm specialization, billings deteriorated further at firms with a multifamily residential specialization, reaching their lowest level since the height of the pandemic in 2020. Firms with a multifamily residential specialization have seen a significant decrease in work over the last nine months. On the other hand, firms with commercial/industrial and institutional specializations reported modest growth this month. However, some fluctuation in business conditions in all sectors is likely to continue over the coming months.

Interest rate hikes likely to pause

Recently there have been some encouraging signs in the broader economy as well. Although inflation remains elevated, the Consumer Price Index (CPI) rose by just 0.4% from March to April—up by 4.9% from one year ago—a significant increase, but still much lower than it was last summer. Notably, inflation in food prices has slowed recently, although gas prices have been increasing again. With the pace of inflation starting to slow, the Federal Reserve chose to raise interest rates by just 0.25 percentage points during their May meeting, to a current target range of 5.0–5.25% and signaled that this may be their last increase for a while.

Strong job gains were cited as one of the reasons why the Federal Reserve may pause their recent increase in interest rates, and nonfarm payroll employment added an additional 253,000 new positions in April. In the architecture services sector, while payrolls have added a total of 3,500 new positions over the last year, employment levels in the industry have generally been flat for the last five months, hovering around 200,000 positions. While this is above the pre-pandemic level of positions, it remains well below the all-time industry high prior to the Great Recession.

Firms reported strong profitability in 2022

This month we asked architecture firms about their profitability in 2022, and how they expect it to change this year. Responding firm leaders reported an average profitability of 10.7% in 2022, with more than half of firms (52%) reporting profitability of greater than 10%, and 12% reporting profitability of 25% or more. Large firms with annual billings of $5 million or more reported the highest profitability levels, averaging 14.8%, while firms located in the Northeast reported the lowest, at 7.6%. In addition, 14% of firms reported a loss for 2022, while an additional 2% reported profitability of 0%.

Overall, a majority of firms expect profitability in 2023 to be either about equal to 2022 levels (37%), or higher (36%). However, more than one quarter of firms (27%), expect their profitability this year to be below 2022 levels, with 8% expecting it to be significantly below 2022 levels. Likely because their profitability was lower in 2022, firms located in the Northeast are most likely to expect higher profitability this year, with nearly half (48%) projecting that it will be above 2022 levels.

When asked about the impact of various factors on their firm’s estimated profitability through the end of this year, firm leaders were most concerned about the potential negative impact of delayed, stalled, and cancelled projects, staff shortages, supply chain issues, and contractor labor shortages. Staff quality and firm morale and culture were most commonly selected as the factors likely to have a very positive impact on firm profitability.

Overall, when firms were asked to select the top three factors that they feel are likely to have a very or somewhat negative impact on their firm’s profitability this year, staff shortages affecting their firm’s ability to meet deadlines and take on new projects and the number of projects that are delayed, stalled, or canceled were the top two factors selected (by 33% and 31% of firms, respectively), followed by staff compensation levels (28%), extended project schedules due to supply chain problems and/or contractor labor shortages (26%), and firm overhead costs (e.g., rent, healthcare, insurance) (24%). Of the factors that firms selected as one of their top three most likely to have a very or somewhat positive impact on their firm’s profitability this year, firm morale and firm culture (31%) and quality of staff (29%) were the top two factors, followed by level of fees negotiated (22%), and marketing and business development activities, and their impact on the number and/or quality of new projects that their firm was able to attract (20%).

What ABI April 2023 Work-on-the-Boards participants are saying

- “We have a lot of healthcare projects on hold awaiting funding or cost reductions to align project scope to budget available.” —150-person firm in the Midwest, institutional specialization

- “Due to labor and material costs, many projects are stopped or canceled. We foresee this trend continuing in our area, which is underserved in the number of available qualified contractors.” —8-person firm in the Northeast, commercial/industrial specialization

- “Pretty neutral. Growth is slowing substantially with the banking crisis.” —42-person firm in the West, mixed specialization

- “Definitely slowing due to funding and delays on owners’ side.” —23-person firm in the South, residential specialization

Join the ABI Work-on-the-Boards panel to participate in our monthly survey. Open to architecture firm owners, principals, and partners. All participants get a free ABI subscription.

The monthly AIA/Deltek Architecture Billings Index is a leading economic indicator for nonresidential construction activity.

Deltek is the home of AIA MasterSpec®, powered by Deltek Specpoint. Deltek helps A&E firms boost efficiencies while improving collaboration and accuracy.

Nearly one quarter of firms report being currently understaffed.

This report reveals how a profession of 116,000 licensed architects enables $693 billion in construction value, supports millions of jobs, and generates a powerful multiplier effect across the